India’s free digital payments revolution has upended how money moves — but not how fintechs make it. Now, Flipkart’s fintech arm Super.money is partnering with one of India’s top commercial banks, Kotak Mahindra Bank, to change that, with an aim to turn usage into profit by bundling UPI payments, savings and secured credit into a single account.

The partnership aims to issue about 2 million secured credit cards in the next 12 months – about 60 percent to first-time borrowers – and 5 million within 2 years. Super.money, which already serves 10 million active users, expects the Kotak alliance to contribute about 10 percent of its revenue next year as it works toward profitability by 2026, Chief Executive Prakash Sikaria said in an interview.

India’s Unified Payments Interface (UPI), backed by the Government of India, has made instant bank transfers free and ubiquitous, processing Over 19 billion transactions A month on, though, that success has left little room for fintech gains, as regulators, including India’s finance ministry, Do not allow merchant fees That usually funds rewards and credit programs. Super.money’s bet — using a secured card and savings account to reintroduce incentives — offers a template for building viable business models on top of no-fee payment systems.

“We do UPI not to solve pure payment use cases,” Sicaria told TechCrunch. “We do UPI to create an attractive cross-financial service play where we are acquiring and retaining customers through UPI.”

Flipkart’s Super money

Launched in June 2024 as Walmart-owned Flipkart’s latest fintech venture after it shuts down PhonePe in 2023, Super.money is already generating monthly revenue of about $3 million with an annual run rate of about $36 million, the executive said.

The fintech app has emerged as one of India’s top five UPI platforms in recent months, processing more than 200 million transactions per month for four consecutive months since August, according to the National Payments Corporation of India, the federal agency that runs the system.

About 80% of Super.money’s revenue comes from personal loans, 10% from credit cards and the remaining 10% from payment products like bill payments and recharges. The fintech says it retains about 85% of users, with 60-70% of its transactions coming from customers under 30 years of age.

TechCrunch event

San Francisco

|

October 27-29, 2025

Sicaria noted that Super.money’s business model relies on two monetization engines. “The first is the financial-services engine — personal loans, cards, deposits and similar products — and the second is commerce,” he said. “Our idea is to bring a Klarna-style ‘pay-in-three’ model to commerce, creating a financial overlay that allows customers to buy now and pay later within the Super.money ecosystem.”

The partnership with Kotak Mahindra Bank, India’s fourth largest lender by market capitalization, gives Super.money access to a large, regulated banking infrastructure. It marks the fintech’s foray into mainstream retail banking, following an earlier deal with Utkarsh Small Finance Bank to offer specially secured cards through its platform.

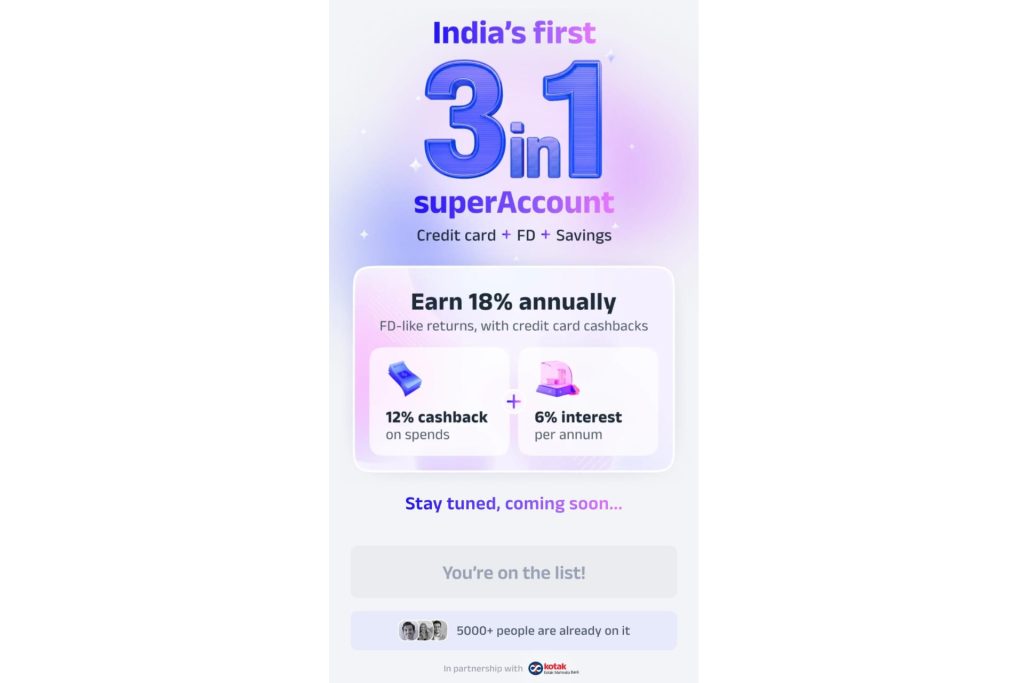

The collaboration aims to expand access to credit for first-time borrowers by combining a savings account, UPI payments and a fixed-deposit-backed secured credit card with what the companies call a “3 in 1 super account.

To open a 3-in-1 super account, users need to make a fixed deposit of at least ₹1,000 (about $11). The account earns interest on deposits and offers a cashback on every transaction. It also has a UPI-on-credit feature — a credit line backed by deposits that requires no income proof.

Sicaria told TechCrunch that the secured cards were chosen as the anchor product because they fit into India’s zero-fee UPI system and still allow for rewards and cashback that the platform was never designed to support.

“Our focus is to bring in users who are more likely to engage with our products,” he said. UPI is the key engagement and acquisition hook, but for people who don’t want to engage with financial services or other products we launch, we don’t want to serve them from a UPI or payment perspective.

After partnering with Kotak Mahindra Bank, Super.money soon partnered with SoftBank-backed Juspay to launch a one-click checkout experience for online merchants, primarily targeting direct-to-consumer brands.

About 1,000 merchants already use the solution, and Super.money plans to expand that network by partnering with more D2C players and other companies within the Flipkart group, Sicaria said.

The secured card earns merchant discount revenue on transactions and provides cashback, Sicaria said. “Of course, there is a standard acquisition fee for the partner bank that we charge to the bank, so that also comes as monetization for us,” he adds.

Super.money plans to issue about 200,000 secured cards per month under the partnership with Kotak before expanding to other banks, Sicaria said.

So far, Flipkart has invested around $50 million in Super.money to start its operations. As the business scales, the fintech plans to raise additional capital — possibly even from external investors.

“We need more capital for at least a few years,” Sicaria said. “Very soon, we will begin formulating our capital raising strategy.”

He declined to say whether the next round would come from Flipkart or outside investors but noted that Super.money is getting inbound interest from “many investors”.

Meanwhile, Sicaria said the company is keeping its cash burn low, describing its current monthly burn as a “low single-digit million number” without saying anything.

He added that Super.money is deliberately focusing on India’s top 10 to 30 million users, rather than competing with mass-market payment players like Google Pay or PhonePe for millions.

“What we want to do is build a strong secured card franchise with a profitable P&L – for us, the bank and also for our customers,” Sicaria said.